.png)

In-cabin 3D Sensing: Market, Competition, Technology, 2021-2030

Active Driver monitoring and Occupant Monitoring System using NIR camera and mmW Radar; in-cabin 3D sensing market for ADAS and autonomous vehicles; OEM, Tier 1, and Tier 2 supplier partnership mapping

Published: 22 Feb 2021

Key Highlights

- Impact of COVID-19 pandemic on passenger vehicle sales, 2021 and beyond

- Design wins of leading active DMS and OMS solutions providers with OEMs and Tier 1 suppliers

- Current and future OEM car models with active DMS and OMS in-cabin 3D sensing

- Total addressable market for in-cabin 3D sensing market for active DMS and OMS

- In-cabin 3D sensing technologies – mmW radar and NIR camera (shipment and TAM value)

- Status of in-cabin 3D sensing market for DMS and OMS across China, United States, and Europe

- TAM and Sales Demand for VCSEL and Photodetectors (APD, SiPM, SPADs)

- Industry Partnerships – DMS and OMS suppliers with OEMs and Tier 1s

- Status of competition between leading Tier 1 suppliers

- Drivers, Challenges, and Opportunities for stakeholders

Exhaustive Coverage

- Passenger Vehicle Sales Trends and Demand along with COVID-19 pandemic impact

- ADAS and Autonomous Vehicle Sales Trends, breakdown by Levels of Automation

- Level 0: No Automation

- Level 1: ADAS

- Level 2: Partial Automation

- Level 3: Conditional Automation

- Level 4: Highway AutoPilot and Park Pilot

- Level 4: Robotaxis

- Market Penetration of Driver Monitoring Systems (DMS), Occupant Monitoring System (OMS), Child detection/presence monitoring in each level of autonomy

- Market Penetration of DMS and OMS across China, US, Western Europe, Japan, S.Korea, Canada, Eastern Europe, Asia Pacific, Middle East & Africa, and South America

- Number of Vehicles equipped with active DMS, OMS, and Child detection/presence monitoring technology

- Market Penetration of NIR camera-based sensing in DMS and OMS Market Penetration of mmW Radar based sensing in DMS and OMS

- Calculated ASPs of NIR Camera Sensing Technology and Radar Sensing Technology

- Market Size by Value of NIR Camera Sensing Technology and Radar Sensing Technology for DMS and OMS Applications

Market Overview

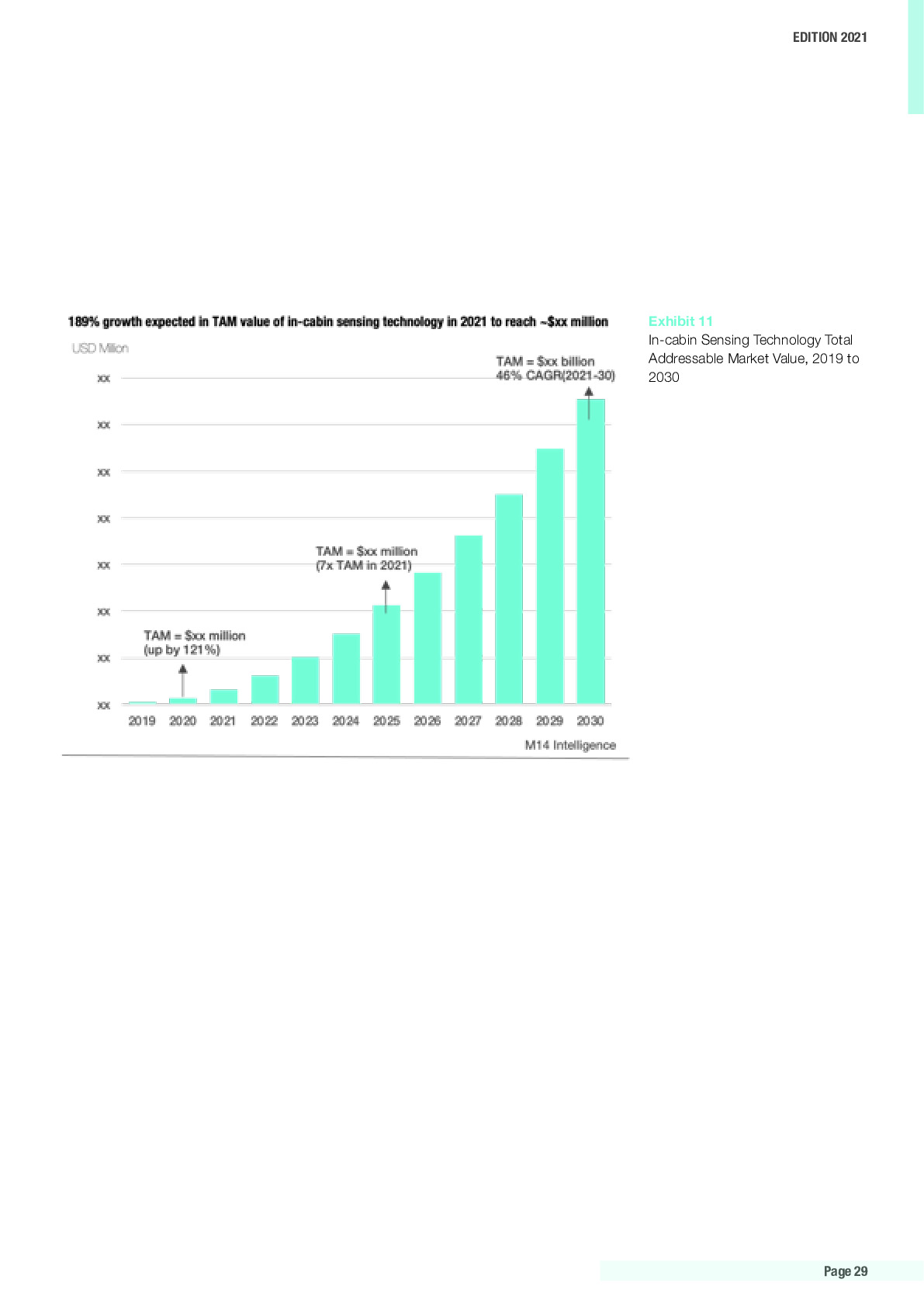

TAM and Forecast

Sample Figures

Key Questions Answered

- Which OEM brands, car models (trim wise) are equipped with active driver monitoring and occupant monitoring system? And what are their sales volume?

- Who are the leading active driver monitoring system and occupant monitoring system technology suppliers? What are their design wins with OEMs and Tier 1s?

- What are the shipments of these leading in-cabin 3D sensing active DMS and OMS suppliers?

- What is the total addressable market (TAM) of in-cabin 3D sensing active DMS and OMS technologies, globally, breakdown by ADAS and autonomous vehicles, and breakdown by geographies?

- What are the ASPs of in-cabin 3D sensing DMS and OMS sensors – NIR camera and mmW radar? What will be the expected price erosion?

- What is the status of driver monitoring (DMS) and occupant monitoring system (OMS) in-cabin 3D sensing technologies in China, United States, and Western Europe?

- What are the differentiating factors of the leading DMS and OMS suppliers in the market?

- How is the status of competition between the leading Tier 1s in DMS and OMS market?

- What are the key driving factors, challenges, and opportunities in the future for in-cabin 3D sensing DMS and OMS market?

- What is the total demand and addressable market for VCSEL, APDs, SiPMs suppliers in the in-cabin 3D sensing DMS and OMS market?

List of Companies

Trademarks are of the respective brands. This is not an exhaustive list. Please download the sample report for more information.

Purchase the study

Individual Purchase

- For 1 user

- PDF copy only

- 1 month post-sales service

- NA

- NA

Company License

- For 2 users

- PDF + Excel

- 1 month post-sales service

- 15% Off on ACES portal subscription

- 8 hours free customization

Enterprise License

- Unlimited Users

- PDF + Excel

- 1 month post-sales service

- 20% Off on ACES portal subscription

- 15 hours free customization

Do you have any specific need?

Let us know your specific requirements

Contact ussales@m14intelligence.com | Worldwide Sales: +1 323 522 4865

Or request a call back !

Related Products

Published : 09 Jun 2025

In-cabin and Exterior Sensing Applications of 4D imaging radar in ADAS and Autonomous Vehicles; 60 GHz, 76–81 GHz, and 140 GHz Band, SAE Level 2+ and ...

Published : 22 Apr 2025

Comprehensive Analysis of Service-Oriented Architecture (SOA), Over-the-Air (OTA) Updates, and Edge Computing in SDVs, Market Estimation and Forecasts...

Published : 28 Mar 2025

Lithium-ion (LFP and NMC) and Emerging Battery Technology (Solid-state and Sodium-ion) Market Sizing, Regional breakdown, Regulatory Policies, Battery...

Published : 05 Mar 2025

Driver Monitoring System (DMS) and Occupant Monitoring System (OMS) using Infrared (NIR), 3D sensing (VCSEL in ToF), Wide-angle Cameras, and Radar; in...

Published : 25 Nov 2024

Market Penetration & Sales Demand of Type of AMR - Inventory Transportation Robots, Picking Robots, Sortation Robots, And Drones for Inventory Managem...

Published : 04 Apr 2023

Autonomous Highway Trucks, Autonomous On-Road Vehicles, Sidewalk Robots/Droid, Market Penetration & Sales Demand, Consumer Analysis, Sensor Content (...

Published : 15 Mar 2023

Inventory Transportation Robots, Picking Robots, Sortation Robots, Collaborative Robots, And Drones; Market Penetration & Sales Demand; Market By Busi...

Published : 10 Aug 2021

In-cabin and Exterior Sensing Applications of 4D imaging radar in ADAS and Autonomous Vehicles; Emerging 4D imaging players competition assessment

Published : 02 Jun 2021

Future of AI powered autonomous precision farming using agriculture robots; RaaS vs equipment sales; driverless tractors; computer vision image recogn...

Published : 21 Apr 2021

Mobile Robots, Sensing, Mapping and Localization Technologies, and Warehouse Automation Solutions Market Analysis, Forecast, and Automation Industry A...

Published : 09 Apr 2021

Container Terminal Automated Equipment, Sensing Technologies, Automation Solutions, and Services Market Analysis and Forecast, Company Assessment, Ind...

Published : 06 Apr 2021

Analysis of 150+ LiDAR companies and total addressable market in the field on ADAS, AVs, Robotaxis, Shuttles, Pods, Construction & Mining, Ports & Con...

Published : 22 Feb 2021

Active Driver monitoring and Occupant Monitoring System using NIR camera and mmW Radar; in-cabin 3D sensing market for ADAS and autonomous vehicles; O...

Published : 14 Oct 2020

Estimated automotive-grade LiDAR mass production timelines, expected pricing at high-volumes, & preferred technology by the leading OEM-Tier1-LiDAR su...

Published : 14 Jul 2020

ADAS and AV development, testing, verification, and validation with Image, Video, Data Annotation, Ground Truth Labelling, Automation Software and Man...

Published : 03 Jun 2020

ADAS and autonomous vehicles enablers shipment, market size, and pricing forecast breakdown by levels of autonomy – camera, LiDAR, radar, V2X, HA GNSS...

Published : 13 Jan 2020

Autonomous vehicles launch timelines by OEMs & robotic vehicle companies (robotaxi, shuttles, pods, long-haul platooning trucks); market penetration &...

Published : 09 Dec 2019

3D sensing camera modules and subcomponents (VCSEL, CMOS image sensor, optics, 3D system design and computing) market penetration, size, shipment, and...

Published : 05 Dec 2019

Cybersecurity application demand and market penetration in connected autonomous vehicles (CAV), pricing/costing models and business models adopted by ...

Published : 03 Sep 2019

Expected mass production timelines of LiDAR for autonomous driving, target cost, LiDAR technologies analysis, LiDAR supplier’s competition assessment ...

Published : 10 Jul 2019

Penetration & Sales Demand (Level 1+2; Level 3 – Highway Autopilot & Long-haul Platooning; Level 4 – Highway Autopilot, Park Assist, Urban Autopilot –...

Published : 15 Sep 2018

Expected mass production timelines of LiDAR for autonomous driving, target cost, LiDAR technologies analysis, LiDAR supplier’s competition assessment ...

Published : 11 Jun 2018

Low & ultra-low power energy harvesting microcontrollers for wearables, medical devices, connected homes, precision agriculture, & smartphones. Blueto...

Published : 25 Jan 2018

Penetration & Sales Demand (Level 1+2; Level 3 – Highway Autopilot & Long-haul Platooning; Level 4 – Highway Autopilot, Park Assist, Urban Autopilot –...