M14 Intelligence ACES division predicts LiDAR shipment from ADAS and autonomous vehicle sensor suite to cross 1.5 million units by 2025 and further expected to grow by 20x by 2030.

One question that keeps on arising over and over in the automotive industry, isLiDAR really necessary? Two major alternative solutions are offered for LiDAR systems - one is the camera based computer vision systems for e.g. of Tesla’s Autopilot and the other is for e.g imaging radar system. Apart from few exceptions the industry quite have common consensus that LiDAR indeed is required for self-driving capabilities. M14 Intelligence asserts that no one particular sensor, but the complete sensor suite needs to be equipped with all the three major sensors including camera, radar, and LiDAR along with ultrasonic for 3D perception and sensing the road environment.

Addressable Market for LiDAR?

To understand what will be the demand for LiDAR sensors in ADAS and autonomous vehicle sensor suite, it is very important to understand where is the actual addressable market. So the question arises what is the actual addressable market for LiDAR sensors? In our earlier analysis (Edition 2019) M14 predicted that LiDAR due to its expensive price could only be integrated in level 3 and above autonomous vehicles. However, the autonomous vehicles industry is volatile and now majority of automakers are exploring the level 2 or level 2+ vehicles market as well for the integration of LiDAR sensors. Clearly, level 3 and above vehicles will need more time in commercialization and deployment due to legislation. And the level 2 autonomy is the best way to get LiDAR technology commercialized in a larger outlook. This will also help in mass production and reduction of per unit LiDAR costs. M14 Intelligence has changed its forecasts by adding L2+ systems in the target market bucket. So the total target market for LiDAR sensor resides in L2+, L3, L4-highway driving consumer purchase vehicles, and L4/5 - robotaxis, shuttles, & pods.

Passenger Vehicles Sales Forecast, Breakdown by Levels of Automation (including robotaxis, shuttles, and pods)

How many LiDARs required?

To identify the total automotive grade LiDAR market the report first identifies the total vehicles that could be integrated with LiDAR sensor as an integral part of its sensor suite and the number of sensors required per vehicle. M14 Intelligence analysis based on the current offerings of LiDAR sensors in both ADAS vehicles and robotaxis, shows that the range might vary a lot. For instance, in an ADAS vehicle minimum of one long-range LiDAR sensor will be integrated while in a robotaxi one to three long-range LiDAR along with 2-6 short range LiDAR could be integrated depending on the OEM requirements. LiDAR companies and their offerings

Estimated number of LiDAR sensors required across L2+/L3, L4-Consumer purchase vehicle, L4-robotaxis

Who will win the race to LiDAR mass production?

Currently the market is full of different technology options across the spectrum with Tier 1s and Tier 2s offerings. More than 100 companies are dedicatedly working on developing the best possible LiDAR sensing system that can be seamlessly integrated with the ADAS vehicles without disturbing the looks and making sure the operational design domain requirements by the OEMs are met. Some of the leading Tier 1 suppliers such as Continental, Bosch, Valeo, Veoneer, Denso, Koito, Magna, Hella, Aptiv, and ZF, among others have already entered the market by either partnering or by M&A strategy with LiDAR manufacturers. Few of the LiDAR manufacturers wish not to have a production line and leaves the manufacturing part with its Tier 1 partner, while focus on technology building.

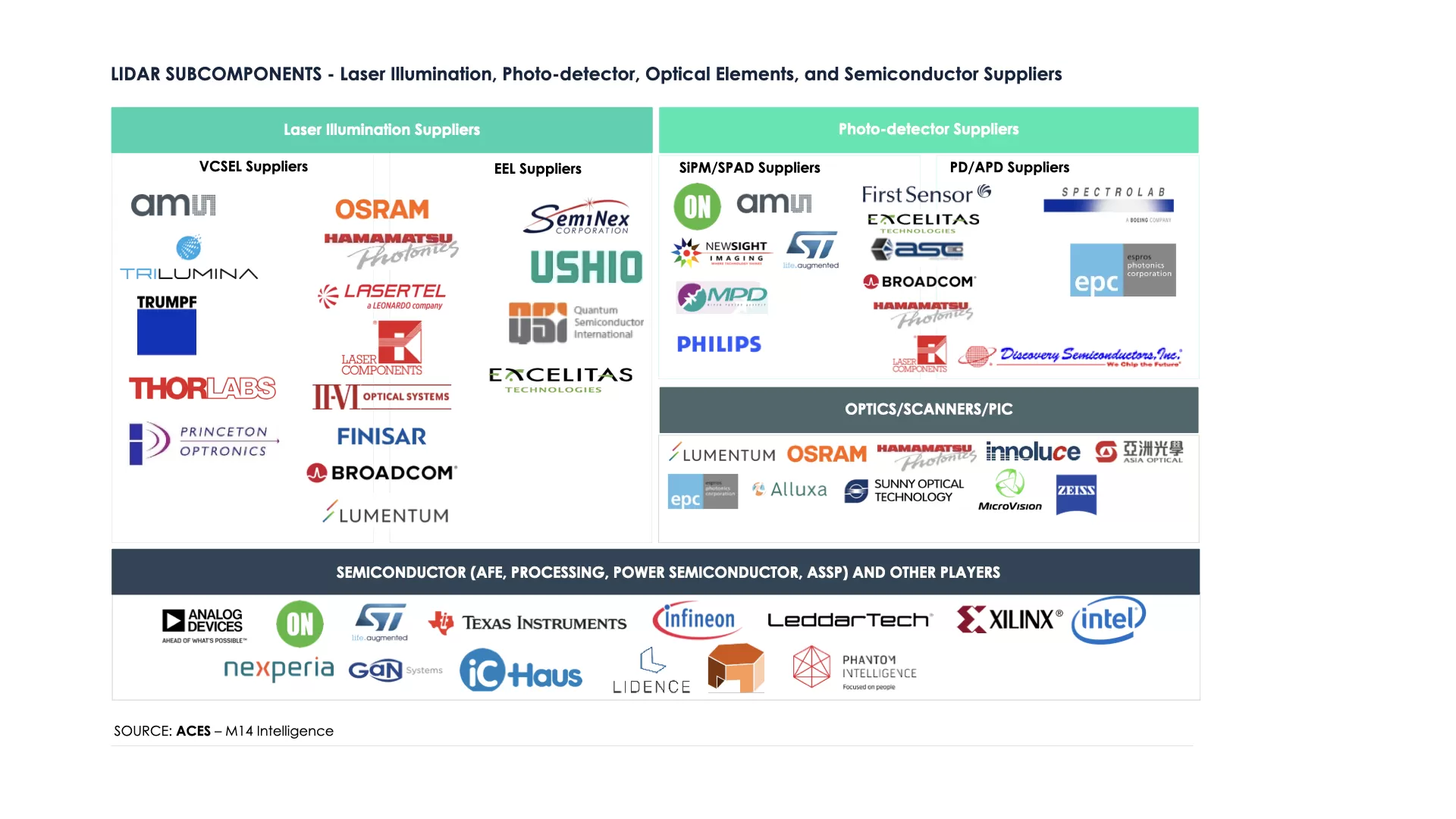

To understand this, M14 Intelligence has analyzed all the players across the LiDAR ecosystem and their technology offerings. At present, the major technologies that are offered are mechanical scanning, MEMS, flash, OPA, e-scanning, and FMCW among others. Along with this the anatomy of LiDAR system is also equally important. Three major components that decides the best fit for automotive application (especially the LiDAR range) is its illumination source, scanning technology, and photo detector. The illumination source wavelength for automotive application is divided - majority of industry uses 905nm while few emerging players are developing 1550nm. The scanning technology that illuminates the scene around a vehicle is of three major types - rotating method (2D or 3D, most famous mechanical scanning), laser & beam steering method (most famous MEMS and OPA), and 2D or 3D flash method. Finally the photodetector technology that detects the reflected light are in the form of APD, SiPM, and SPAD. The company that could offer long-range, low-reflective - bright sunlight operation, excellent resolution, that could easily blend with the aesthetics of a vehicle, and top of it be pocket friendly (especially below $500 for long-range and close to $100 for short-range application) will win the race. The report published by M14 Intelligence on LiDAR market gives a detailed analysis on the comparison of all the leading brands across the LiDAR ecosystem on the above mentioned parameters.

LiDAR Manufacturers researched during the course of research

The cost of LiDAR depends on its laser/illumination source, photodetector array, optics, housing, FPGA/ASIC, thermal management, and AFE, along with manufacturing cost among others. However, illumination source and photodetector are two major components that occupy the larger section of the BOM. The illumination source accounts for more than 80% of the cost of a 64channelmechanicalscanningLiDAR905nm while APD array costs around 10%. With mass production the cost of such LiDAR could come down to less than $1,000 by 2025 and by most optimistic view to $600. The other example could be of a 1550nm mechanical scanning LiDAR with 1 channel (which currently is 10-100x more expensive than 905nm LiDAR) occupies ~20% and 4 channel InGaAs APD which accounts for more than 75% of the total cost of the LiDAR system. The cost of such LiDAR can fall down to less than $800 or by most optimistic view to $600 by 2025 if mass production is achieved. Third example could be of a 1550nm mechanical scanning 128-channel LiDAR with 905nm VCSEL (~40-45% of BOM) and SPAD array (~40-45% of BOM) with e-scanning. Such LiDARs are cheaper currently and with mass production could cost less than $300 or by most optimistic view less than $150 by 2025.

The future of LiDAR market in automotive industry

The LiDAR technology witnessed huge marketing in recent years and big promises were made by some of leading players. Ultimately, it all depends on the legislations in terms of demand for autonomous vehicles and robotaxis. While the demand in level 2+ vehicles could be promising provided that the companies focus on trying to 1.reduce the cost and 2. blend the LiDAR system in the vehicle body. Secondly the standardization of range testing of LiDAR needs to in place. The industry has already witnessed billions of dollars of investments and M&As in the LiDAR industry besides, this year was phenomenal with companies announcing IPOs and entry of new big brand. And finally the AI and software competence along with LiDAR is also very important for players to win this race.

In-cabin monitoring technology has rapidly evolved, becoming a critical feature in modern vehicles. At CES 2025, industry leaders such as Smart Eye, ...

The in-cabin monitoring technology sector is poised for continued growth, driven by technological advancements, regulatory mandates, and increasing c...

.png)